Home equity is the largest asset class for approximately two-thirds of American homeowners. Home Equity Contracts (“HECs”) are a relatively new financial tool for homeowners to monetize their home equity without the burdens of traditional debt financing.

HIGHLIGHTS

- An exceptional chance to gain access to primary mortgages, offering a unique investment opportunity.

- Minimal, if any, association with the fluctuations of public markets.

- Demonstrated history of attractive returns.

- Promising catalysts that have the potential to generate significant short-term profits.

INTRODUCTION

Home Equity Contracts are an emerging investment asset class, with attractive unlevered returns, capital gain tax treatment, built in downside protection, and broad geographic diversification throughout the top metropolitan statistical areas (“MSA’s”) in the U.S. Residential Real Estate Market.

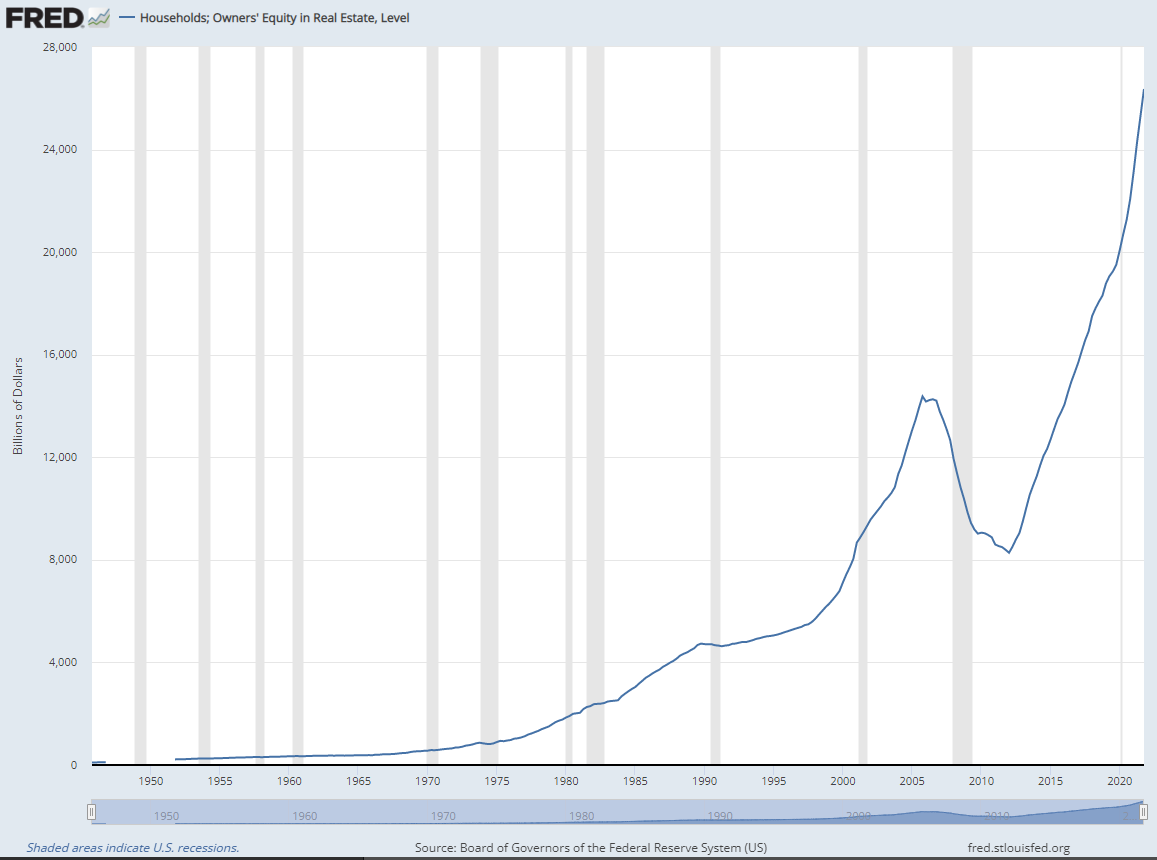

U.S. homeowners are house rich and cash poor and for about 67% of American homeowners, home equity is the largest asset they own. To better explain the potential for the HEC market, home ownership in the U.S., as of 2019 was 65%. Further, the primary residence continues to as the largest asset among households across various age groups, racial and ethnic demographics. Overall, the home equity market in the U.S. is valued at $30 trillion. The chart below shows the growth in homeowners’ equity from 1945 to the present. Further, this chart illustrates the resilience of home equity through numerous recessions, the exception being the 2008 GFC which was largely a housing driven crisis.

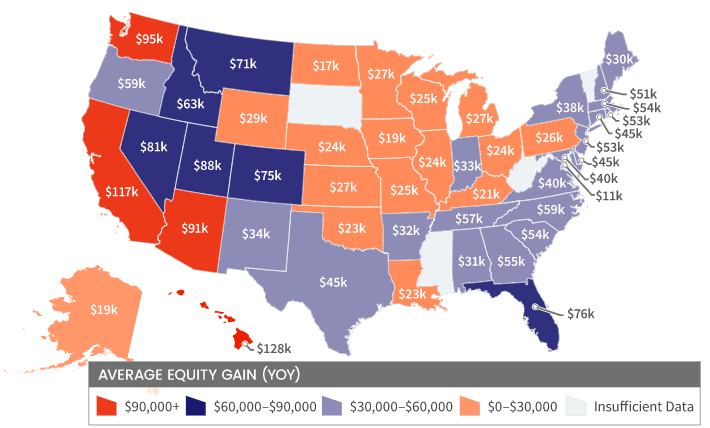

CoreLogic estimated the growth in home equity at over $3 trillion for Q1 of 2021 alone. The breakdown of these gains, by state are illustrated in the chart below.

On the demand side, consumers have many reasons for needing liquidity. The largest such reason, when it comes to HECs, appears to be debt reduction. Other reasons include renovations, investments, business starts, and life events such as, divorce, education, and medical expenses

HISTORY

In the past, homeowners could only sell their entire home or borrow against the value of their home to get liquidity.

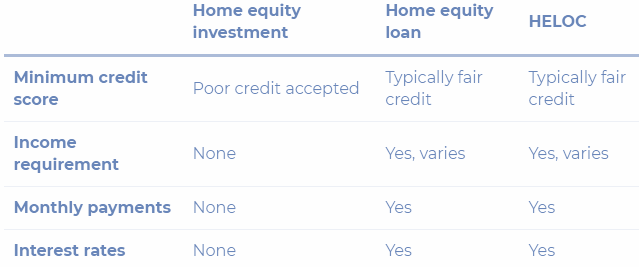

This chart provides a quick overview of why HECs are growing in popularity as an alternative to traditional mortgage refinancing and HELOCS.

For comparison and context, there was $262 billion of HELOC originations in 2021. Similarly, there were $13.2 billion of reverse mortgage originations. The HEC originations over this same period were approximately $500 million. The graphic below highlights why an HEC might be preferrable for a homeowner relative to other liquidity options (the same would likely mitigate any regulatory risk).

HOW IT WORKS

The HEC enables homeowners to monetize home equity by selling an equity participation in their home to an investor. The HEC is generally structured as an option agreement. The homeowner receives the HEC dollar amount while the investor gets a percentage of the current home value and a participation in any future change in the value of the home, for the term of the contract.

Investors get downside protection and upside participation while investing in tangible real property. The investor’s downside protection comes primarily from purchasing a “share’ of the home at a discount to the appraised value of the property. The investor also has an accelerated participation in any future change in the value of the home. The Home Equity Contract includes a lien on the home in favor of the investor and the homeowner has an obligation to abide by the terms of the contract. The homeowner receives immediate liquidity without incurring debt or selling their home, and if the home appreciates, the homeowner’s remaining equity is worth more, and the investor’s Home Equity Contract is worth more. If the home loses value, the homeowner’s remaining equity is worth less and the investor’s Home Equity Contract is worth less if the loss exceeds the initial discount or risk adjustment.

The Homeowner controls the duration of the contract and can buy out the contract by refinancing the home, selling the property, or using other funds to settle the contract. Typical HECs involve a home with 40% to 50% of equity.

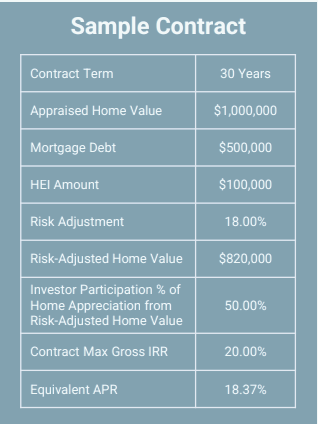

Contracts are now predominantly 10 or 30 year tenors. It is not uncommon for a “risk adjustment” to be 15% – 25% below the appraised home value. Similarly, the upside participation is typically asymmetric (due to the risk-adjusted home value); in this example 50%. This of course is mitigated by the profit cap put in place within the contract in the form of a maximum gross IRR. The contracts max amount (i.e. how much the owner will receive) is limited to 25% of the equity in the home.

In several states, homeowners can be precluded from taking on additional debt (post-HEI). In other States, it is written into the contract that no debt may be added which is senior to the HEC owner’s equity. This has the same effect as precluding equity as no bank should be willing to provide debt that is subordinate to equity.

By using data analysis and software-driven origination platforms, Home Equity Contract Originators can identify the properties and homeowners that are attractive candidates for Home Equity Contracts. Home Equity contracts are currently available in 28 states plus Washington, D.C. and this number is expected to continue to rise. Origination volume is increasing as contract origination companies scale their platforms and attract investor capital to this new investment asset class.

There are approximately 7,500 county recorders. Originators develop programs to go online and see homeowner’s debt, credit card balances, etc. and send targeted ads (Google, Facebook, etc.) and e-mails. It’s estimated that around 12% of homeowners who go through the originator’s website will end up in a contract.

Originators analyze data to identify HEC candidates and they underwrite the home and homeowner. Some factors they will consider as part of the underwriting process include:

- Home Homeowner

- Geographic & economic factors Equity in the home

- Local wage growth Use of proceeds

- Sale history of home Lien position

- Appraisal value Debt to income ratio

- Occupancy Cash reserves

- Stress test of home price (GFC) Standard mortgage underwriting metrics

The credit assessment and due diligence process that is undertaken before a Home Equity Investment is originated includes traditional lending underwriting standards, which are utilized to assess the homeowner and home. On average it takes 30 days from the identification of a potential homeowner to the origination of the Home Equity Investment.

Generally, originators collect 3% from homeowners as a one-time origination fee, collect a fee from purchasers of the HECs and get paid 1% annually for the life of the contacts for servicing, and receive 5% of profits at the end of the contracts.

INVESTMENT FUNDS

To take advantage of the opportunities in this space, there are investment funds that specialize in creating diversified portfolios of structure Home Equity Contracts. These portfolios are structured so that, if one contract fail to perform at its end it is highly unlikely to have any material impact on the overall performance of the fund. This is due to 3 main factors:

- A high volume of contracts - so that the impact of any single Contract on the aggregate performance of the fund will be minimal.

- Geographical diversification - so that any event that adversely affects a homeowner in one state is very unlikely to do so in another and again only a small portion of the fund will be affected.

- Homeowner diversification – so that if one homeowner should default say, due to bankruptcy, it will not affect the likelihood of another homeowner defaulting. Also, since HECs are designed for homeowners with a considerable amount of equity already in their home, the number of homeowners who might experience financial hardship should be limited and a small number of individual cases shouldn’t have a significant outcome on a diversified portfolio of contracts.

CONCLUSION

There is potential for significant growth in this relatively new space given that home equity is increasing while at the same time mortgage and HELOC rates are increasing which should result in fewer home sales and less HELOC demand (as homeowners seek an alternative). Given their attractive unlevered returns and limited downside risk, HECs and funds that invest in them can be appealing investment opportunities.

This document and the information contained herein is not and must not be construed as an offer to sell securities and is qualified in its entirety by the fund’s private placement offering memorandum. Certain statements included in this presentation, including, without limitation, statements regarding the fund’s investment goals, underlying investment strategies, and statements as to the investment adviser’s beliefs, expectations or opinions are forward-looking statements within the meaning of section 27a of the securities act of 1933 (the “Securities Act”) and section 21e of the securities exchange act of 1934 (the “Exchange Act”) and are subject to risks and uncertainties. The factors discussed herein and throughout this presentation could cause actual results and developments to be materially different from those expressed in or implied by such forward-looking statements. Accordingly, the information in this presentation cannot be construed as to be guaranteed.

Privately offered investment vehicles commonly called hedge funds or private equity funds (“Private Funds,” which include fund of funds) are unregistered private collective investment funds that invest and trade in many different markets, strategies, and instruments (including securities, non-securities, and derivatives). There are substantial risks to investing in Private Funds. You could lose all or a substantial portion of your investment in a Private Fund. You must have the financial ability, sophistication, experience, and willingness to bear the risks of an investment in a Private Fund. An investment in a Private Fund entails risks that are different from more traditional investments and is not suitable or desirable for all investors. Only qualified eligible investors should invest in Private Funds. You should obtain investment and tax advice from your advisers before deciding to invest.

The Fund(s), General Partner, and Investment Adviser have not been recommended or endorsed by any federal or state securities commission or regulatory authority. Furthermore, the foregoing authorities have not reviewed this document and as such have not confirmed the accuracy or determined the adequacy of this document. Any representation to the contrary is a criminal offense.

Any statements about, or presentation of, performance information relating to KPC Funds or Underlying funds or indices are presented for illustration purposes only and are not intended nor may they be construed as indications, predictions, or projections of future performance of the fund or any manager. The fund(s) may be newly formed and may have little or no historical performance record, and the performance data presented herein may not be considered a substitute for the fund’s lack of historical performance.