Bank consolidation in the United States shows no signs of slowing down; in fact, it is expected to gain momentum. This surge in consolidation is driven by various market factors that are shaping the banking landscape.

Highlights

- The U.S. is estimated to have has many domestic banks as the rest of the world combined.

- Bank consolidation is poised to maintain its momentum and even gain speed in the future.

- We believe the optimal way to exploit these community and regional banking trends is through an event driven, long/short investment strategy focused on the community and regional banking sectors.

An Accelerating Trend

Bank consolidation within the U.S., specifically among regional and community banks, is a long-term trend buoyed by common sense macroeconomic drivers. However, when banks combine there is typically a winner and loser (or at least a lesser winner). In this post, we will explore these consolidation trends and how one might gain exposure to such trends from an investing perspective.

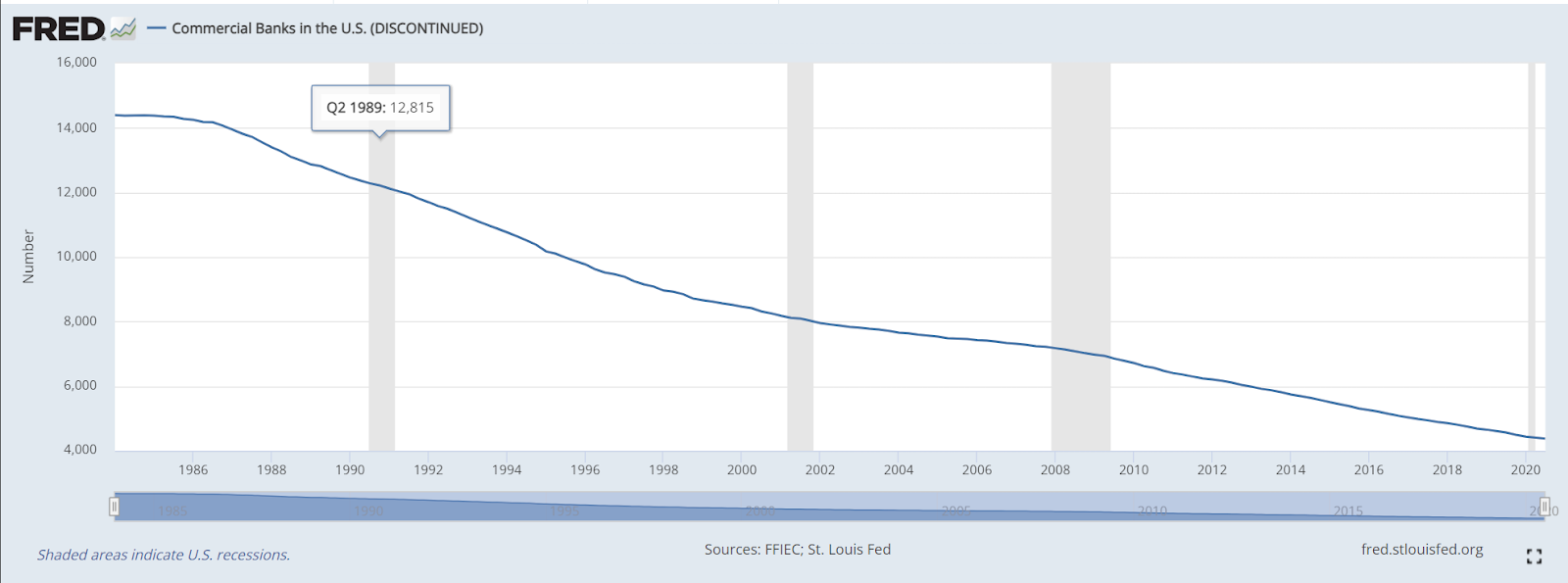

It appears bank consolidation will not only continue in the U.S. but will also accelerate. This acceleration will be a function of several market factors, some relatively new; some which have been driving consolidation for years. The chart below, from the Federal Reserve, shows the declining number of U.S. banks. One might question if this trend will continue or if we may have already bottomed out in this regard.

First, let’s understand the context in which this consolidation is taking place. The U.S. is estimated to have has many domestic banks as the rest of the world combined. The chart above indicates north of 4,000 commercial banks. Add to this the nearly 1,000 savings intuitions and there are well over 5,000 banks in the U.S. (as of Q2 2023).

While assets are concentrated among the U.S. largest banks (approximately 50% at the largest commercial banks) the U.S, stands out among other developed countries with its industry fragmentation. To reiterate, the U.S. has more than 6,000 commercial banks and savings institutions. To put this in further context, as of September 2016, Canada has 30 domestic banks. France has 9 domestic banks.

According to the IMF, there were 30.53 commercial bank branches in the U.S. per 100,000 adults. As of the end of 2022, the number was 27.20; a nearly 11% decline in just 3 years. By contrast, Canada, at the end of 2022 (a) had the same number of commercial bank branches in the U.S. per 100,000 adults as they did in 2019 and, (b) nearly 30% fewer than the U.S.

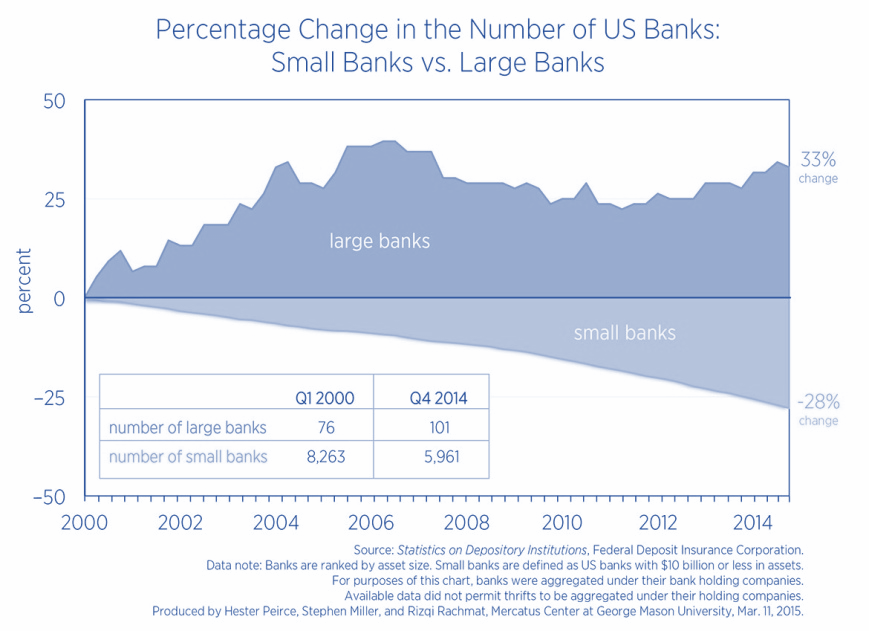

The chart at left speaks to how the decline in bank numbers is historically driven by consolidation with larger and regional banks acquiring smaller banks as these smaller community banks struggle with low net interest margins brought about by years of declining rates, increased regulatory and technology compliance costs, and post-2008 balance sheet health making M&A more plausible. As community banks are limited to working within their community, often expansion is only possible through M&A or becoming a target of a larger acquirer.

The consolidation will continue in the U.S. driven by several market factors. The pace of this long-term consolidation trend will be especially accelerated among smaller community banks.

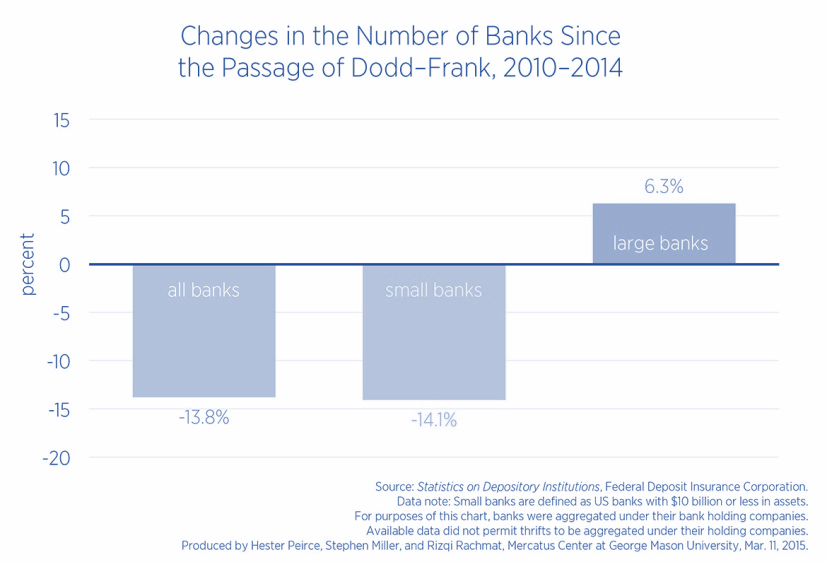

- The cost increases brought on by regulatory demands and technology investments argue for scale and efficiency. Post 2008/9 market crisis, banks have been faced with Basel III and Dodd-Frank Act requirements such as stress testing, along with building out compliance functions, notably around Bank Secrecy Act and anti-money laundering, as well as overall consumer compliance. While some efforts have been made to shield smaller banks from the full scale burden of this legislation, it has not gone nearly far enough. The chart right speaks to the regulatory burden on banks and the broad industries reaction. Add to this the cyber-security threats of today and competition from on-line, non-bank, lenders and even smaller banks are compelled to invest in technology. While this investment may bring long term efficiencies, it often requires a significant upfront investment in what is already a profit-pressured environment.

- Post-downturn balance sheets have been nursed back to health, shifting the focus back to growth and execution upon longer term strategic visions.

- Additionally, the macroeconomic environment is fostering a consolidation-conducive environment, a recent article states, “With all the discussion surrounding the Federal Reserve’s recent interest rate lift-off, consolidation in the banking sector is also set to accelerate.” This of course, comes after years of declining net interest margins, driven by low rates, forced banks to seek profitability through scale and thus acquisition. “Bank margins fell to 3.02 percent in the first quarter of 2015, the lowest average net interest margin since 1984 according to the FDIC…Banks will need a steepening yield curve in order to genuinely benefit from rate rises. What is sometimes overlooked is that interest rates have been on a fairly steady long-run decline since the early 1980s, pocketed by a only a few up cycles over that time period.”

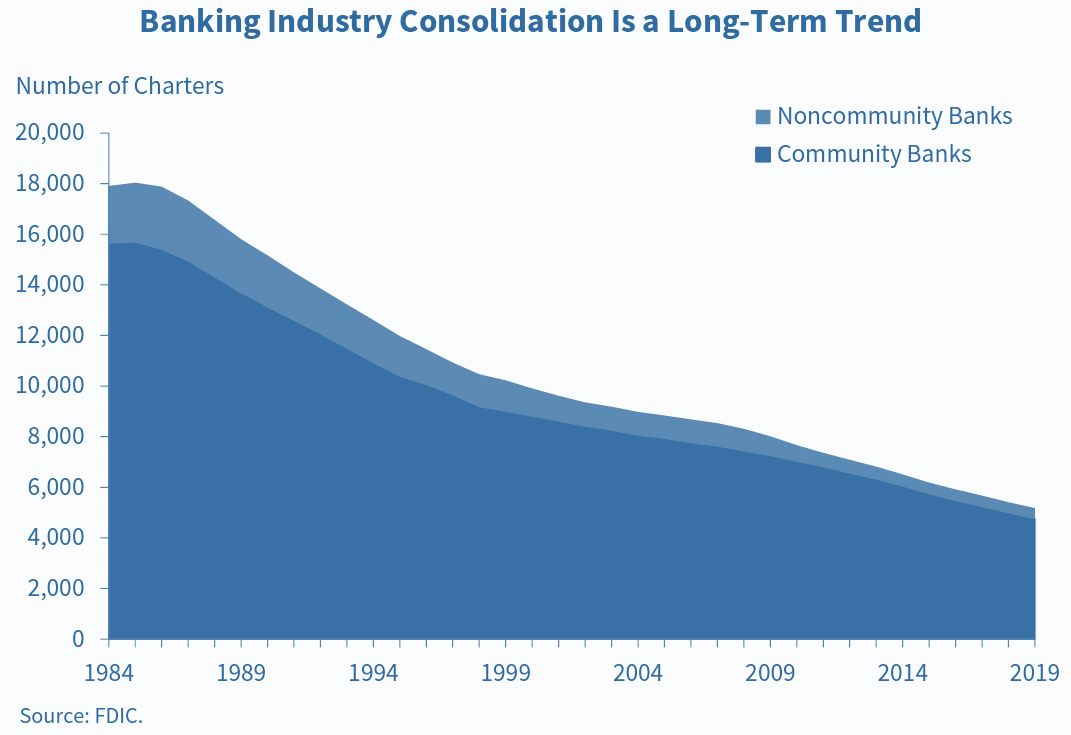

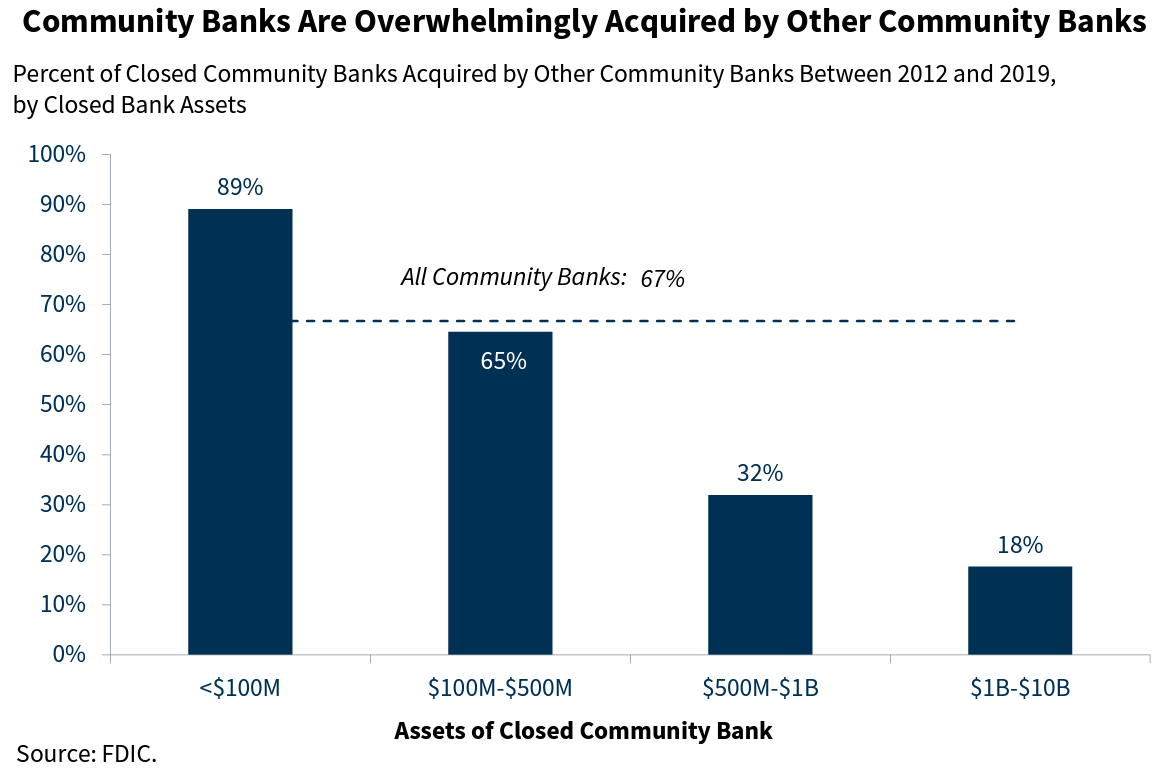

Bank consolidation in the U.S. is a long-term trend and one that will continue, spurred on by the factors referenced above. A Q3 2020 presentation by the FDIC Advisory Committee of State Regulators focused specifically on the tends within community bank consolidation, concluding that “Banking industry consolidation is along term trend” and “Community banks are overwhelmingly acquired by other community banks.” These conclusions are further supported in the charts below.

Conclusion

KPC believes the optimal way to exploit these community and regional banking trends is through an event driven, long/short investment strategy focused on the community and regional banking sectors. Such a strategy may capitalize on the ongoing consolidation in community and regional banks by investing in banks that have a higher probability of being taken out with a high premium and shorting banks that have a low assessed probability of takeover and a lower likely premium if they were to be acquired. Within this concept is the potential for a merger arbitrage sub-strategy during times of higher levels of takeover activity as many of the community bank mergers make use of warrants and embedded optionality through cash versus stock elections as well as collars on the exchange ratio or collars on the fair value received.

If you would like to learn more about these trends and our opinions on how best to gain exposure to them, please contact us.

This document and the information contained herein is not and must not be construed as an offer to sell securities and is qualified in its entirety by the fund’s private placement offering memorandum. Certain statements included in this presentation, including, without limitation, statements regarding the fund’s investment goals, underlying investment strategies, and statements as to the investment adviser’s beliefs, expectations or opinions are forward-looking statements within the meaning of section 27a of the securities act of 1933 (the “Securities Act”) and section 21e of the securities exchange act of 1934 (the “Exchange Act”) and are subject to risks and uncertainties. The factors discussed herein and throughout this presentation could cause actual results and developments to be materially different from those expressed in or implied by such forward-looking statements. Accordingly, the information in this presentation cannot be construed as to be guaranteed.

Privately offered investment vehicles commonly called hedge funds or private equity funds (“Private Funds,” which include fund of funds) are unregistered private collective investment funds that invest and trade in many different markets, strategies, and instruments (including securities, non-securities, and derivatives). There are substantial risks to investing in Private Funds. You could lose all or a substantial portion of your investment in a Private Fund. You must have the financial ability, sophistication, experience, and willingness to bear the risks of an investment in a Private Fund. An investment in a Private Fund entails risks that are different from more traditional investments and is not suitable or desirable for all investors. Only qualified eligible investors should invest in Private Funds. You should obtain investment and tax advice from your advisers before deciding to invest.

The Fund(s), General Partner, and Investment Adviser have not been recommended or endorsed by any federal or state securities commission or regulatory authority. Furthermore, the foregoing authorities have not reviewed this document and as such have not confirmed the accuracy or determined the adequacy of this document. Any representation to the contrary is a criminal offense.

Any statements about, or presentation of, performance information relating to KPC Funds or Underlying funds or indices are presented for illustration purposes only and are not intended nor may they be construed as indications, predictions, or projections of future performance of the fund or any manager. The fund(s) may be newly formed and may have little or no historical performance record, and the performance data presented herein may not be considered a substitute for the fund’s lack of historical performance.